MIFIDPRU 8 Disclosure and Policy for an MIFIDPRU Investment firm at 31st December 2023

INTRODUCTION

Regulatory Context

Multrees Investor Services Limited (the Firm) is a non-SNI MIFIDPRU Investment Firm which is regulated under the Investment Firms Prudential Regime (IFPR) with effect from 1 January 2022. The Disclosures replace the previous Pillar 3 Disclosures.

The document is informed by the Internal Capital and Risk Assessment (ICARA) document and process therein. The ICARA document is kept under review and subject to annual formal revision and approval.

The Firm is a specialist provider of consolidated reporting and investment administration services to investment managers and custody services to the underlying customers of those clients.

Incorporated as a Limited Company in England and Wales in 2010, the Firm became authorised and regulated by the FCA on 5 January 2011.

The Firm does not make investments on its own behalf and does not operate its own trading book.

Scope and Application of MIFIDPRU Disclosure Requirements

This document has been produced by the Firm to meet the disclosure requirements under chapter 8 of MIFIDPRU of the FCA Handbook. The Disclosures related to the year ending 31 December 2022.

Frequency of Disclosure

The Firm will be making MIFIDPRU disclosures at least annually on the date it publishes its annual financial statements. The Disclosures are as at the Accounting Reference Date which is the last day of the calendar year and any figures included in this document will be based on the audited accounts as at that date.

Location of Disclosure

The Disclosures are published on our website (www.multrees.com).

Verification

The Disclosure below is made for the purpose of the Firm complying with the applicable MIFDIPRU 8 disclosure requirements and should not be used for any other purpose.

Materiality & Confidentiality

The Firm regards information as material in disclosures if its omission or misstatement could change or influence the assessment or decision of a user relying on that information for the purpose of making economic decisions. If the Firm deems a certain disclosure to be immaterial, it may be omitted from this Disclosure.

Investment firms may omit required disclosures where they believe that the information is proprietary or confidential. The Firm regards information as proprietary if sharing that information with the public would undermine its competitive position. Proprietary information may include information on products or systems which, if shared with competitors, would render the Firm’s investments therein less valuable. Further, the Firm must regard information as confidential if there are obligations to customers or other counterparty relationships binding the Firm to confidentiality. The Firm has made no omissions on the grounds that it is immaterial, proprietary or confidential other than as may be disclosed in the statutory accounts.

Proportionality

In complying with the rules in MIFIDPRU 8, the Firm has adhered a level of disclosure that is appropriate to its size and internal organisation, and to the nature, scope, and complexity of its activities.

Governance Structure

The Firm is committed to good risk management and prioritises risk management through its functional structure, governance processes, monitoring and reporting activities and its emphasis on the Firm’s vision and values.

Governance Bodies

1. The Board

From the Board down, the Firm considers its risk appetite in its strategy, business plans and risk management process. Overall, the Board monitors and oversees the Firm’s operations, ensuring competent and prudent management, sound planning, proper procedures for the maintenance of adequate accounting and other records and systems of internal control, and for compliance with statutory and regulatory obligations.3

2. The Audit and Risk Committee

The Board has established the Audit and Risk Committee (ARC) and has delegated responsibilities documented in a detailed Terms of Reference. The ARC is chaired by one of the Non-Executive Directors (NEDs) and membership includes two NEDs, the Executive Director, the Chief Risk and Compliance Officer and the Compliance Manager. The ARC advises the management body on the Firm's overall current and future risk appetite and strategy and assists the management body in overseeing the implementation of that strategy by Senior Management. Overall responsibility for management of risks remains with the CEO and the Firm’s management.

3. The Remuneration Committee

The Firm is not required to have in place a remuneration committee. However, the Firm has put in place a Remuneration Committee (RemCo). RemCo has responsibility for oversight of remuneration across the entire firm. The Remuneration Policy is risk-focused, helping to identify and manage risks and promoting a strong risk culture within the Firm.

Governance Bodies – Operational Level

1. Risk Committee

The Firm is not required to have in place a risk committee. However, the Firm has put in place a Risk Committee. The Risk Committee is tasked with overseeing the operation of the Multrees Risk Management Framework on a day-to-day basis. The Risk Committee advises the ARC on the firm's overall current and future risk appetite and strategy and assist the ARC in overseeing the implementation of that strategy.

2. CASS Governance Committee

The CASS Governance Committee is responsible for the oversight of compliance with the FCA CASS sourcebook rules and guidance. It operates under the auspices of the Executive Director assisting in his discharging of his CASS Operational Oversight responsibility. Day-to-day responsibility for the committee sits with the Risk team. Membership consists of senior managers across the various Operations functions, together with the Risk and Compliance Managers.

Directorship as at 31st December 2022

The list of executive directors for the Firm are noted below:

A. David Nicol Chairman of the Board and Non-Executive Director

B. Elaine Clements Non-Executive Director

C. Magnus Carlsson Non-Executive Director

D. Chris Fisher Chief Executive Officer

E. Clive Stelfox Executive Director

Diversity and Inclusion

The Company is committed to being an equal opportunities employer and preventing illegal discrimination in employment. It is the Firm’s policy that:

A. Only the most suitable individuals are to perform the respective senior / (non)executive roles.

B. A diverse culture allows the Board and senior managers to effectively assess the direction of the Firm and each decision made.

C. The Firm is committed to maintaining a diverse blend of members across the business, including its management body.

D. The Board has zero tolerance in respect of unfair treatment or any kind of discrimination, both internally as well as in relation to clients, customers and any third parties.

Risk Management Objectives and policies

Risk Management Framework

Risk management within the Firm is based on a ‘three lines of defence’ model, as follows:

First line of defence (business management and staff) - responsible for identifying and assessing the risks faced in the business and ensuring that appropriate controls are established and maintained. This is overseen and strengthened by the Risk team.

Second line of defence (Risk & Compliance) - responsible for establishing an effective policy framework for the business and conducting compliance monitoring.

Third line of defence (Internal Audit) – provides independent and objective assurance on the effectiveness of risk management, control and governance processes. Multrees does not have an internal audit function therefore this activity is outsourced to a third party to provide an equivalent service.

The Firm is committed to on-going review and development of all three lines of defence in line with its businesses scale and risk profile.

The Firm’s Board meets in person at least quarterly with additional calls as and when required. The Board is made up of executive and non-executive directors, with at least one independent non-executive director. A Board pack is circulated in advance of each meeting to be reviewed and challenged as appropriate. The Board pack contains relevant and timely information in sufficient detail to enable the Board to understand the business and assess the risks, including the on-going assessment of the adequacy and quality of capital and liquidity. The management accounts are included in the Board pack and presented compared to budget after each quarter end.

On-going risk reporting provides the Board, the ARC and senior management with risk management information concerning the Firm’s risk exposure. This information also forms part of the Firm’s ICARA document. The Firm is committed to managing the applicable risks to the business and maintaining an effective internal control structure which includes oversight, monitoring and reporting of risks. Through independent lines of reporting for risk oversight and operations, our risk governance policies are designed to provide objective assessments and monitoring of risks. Management regularly reviews the level of risk it regards as appropriate in order to operate within its regulatory obligations and achieve it business objectives.

Risk Appetite

The Firm aims to develop systems and controls to mitigate risk to ensure they remain within the documented risk appetite.

The Firm sets its risk appetite by considering the material risks in the business and then evaluates the level of acceptable risk, either subjective or objective, and the related measurements. Any risk exceeding the risk appetite will be reported to the ARC along with the action plans to bring the risk back within tolerance.

For those key risks which cannot be managed the residual financial risk is quantified and included in the ICARA document through the Firm’s assessment of its own funds threshold requirement and additional capital may be held against it.

Key Risk Categories

The Firm considers its operations to be prudent and risk averse, with the business objective of achieving client satisfaction and financial strength of the company. The Firm is exposed to risks inherent in the Firm’s business and activities. The Firm has risk management policies, practices and reporting in place for each category of risk it is exposed to. All of the Firm’s risks are addressed via the ICARA document and the Firm’s Risk Management and Governance Framework.

Through the ICARA process, the Firm has applied the relevant K-Factors which are relevant to its business model.

A number of key risks associated with the Firm’s activities, which have been assessed via the ICARA process, are listed below:

A. Credit Risk- The Firm’s main exposures to credit risk is the risk that custody and administration fees cannot be collected, and cash held with banks. The Firm holds corporate cash with banks assigned high credit ratings. The Firm carries out initial and on-going due diligence on new clients, including assessment of their credit risk, and all of the current clients are appropriately regulated, further reducing our exposure to credit risk. Credit risk exposure is therefore considered low and can be mitigated by process controls and, if necessary, can be funded from its capital and liquidity provisions.

B. Market Risk- is the risk of loss due to adverse changes in the financial markets. The Firm does not trade on its own account, so exposure is limited. However, capital market fluctuations can have an effect on client activity and Assets Under Custody (AUC). Revenue earned by the Firm will be impacted by overall market performance and prices due to the practice of levying fees as a percentage of AUA. However, comparison of historical market movements against revenue has shown that the impact on the Firm is less than actual market movements, due to a combination of minimum fees and the expertise of the Wealth Manager clients. The Firm also has a limited exposure to market risk through foreign currency exchange rate movements for any assets held on the Firm’s Balance Sheet denominated in a foreign currency. Market Risk is mitigated therefore through the pricing structure and underlying client base, and exposure is therefore low.

C. Settlement Risk- The Firm does not offer contractual settlement to customers so has no settlement risk. Multrees does provide a FFX service, but this is provided as a matched principal and settlement risk is mitigated contractually as far as possible.

The Firm does not run a trading book or take proprietary positions. Notwithstanding this, the Firm has implemented a risk management framework to remove or mitigate the risks inherent in its business and associated with operation errors, including administrative errors, process failures, loss of IT services and competence and negligence of employees. This recognises that operational risk is a significant risk area within the Firm if not carefully managed. The Firm uses its Risk team to reinforce and oversee the operation of these controls and the risk framework. If required, third parties may also be engaged to undertake independent reviews as a third line of defence. The operational risk framework in place to mitigate operational risks includes:

· Errors reporting, reaction and management to ensure root cause and preventative actions are investigated and implemented promptly by the business

· Reporting and analysis of risk issues to the ARC and the Board

· Operational and Strategic level risk registers to identify and address risks to operational and strategic objectives

The Board is satisfied that all foreseeable operational risks can be adequately mitigated. mitigated by the respective process controls, and where necessary, can be funded from capital provisions under the Firm’s Pillar 2 financial resources.

D. Concentration Risk- The Firm has identified the following areas where concentration risk can arise:

a. Positions and exposures

b. Location of client money

c. Location of client securities

d. Location of Firm’s own cash

e. Earnings

The Compliance, Risk and Finance departments of the Firm monitor the above areas on a monthly basis to ensure that no concentration risk arises.

Multrees has a limited licence to deal in investments as principal in the capacity of a matched principal broker.

Overall, the Firm’s concentration risk has been assessed as low.

CAPITAL RESOURCES AND REQUIREMENTS

Own Funds

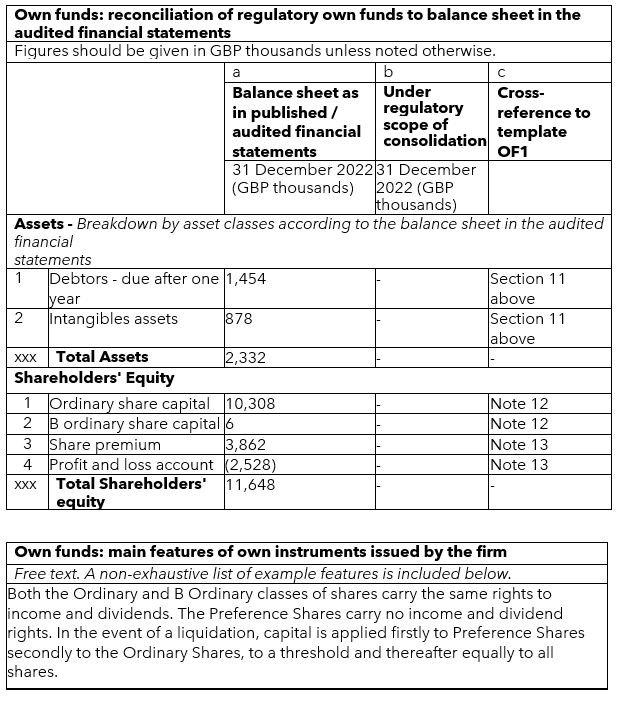

This disclosure has been made in accordance with the MIFIDPRU 8.4 requirements using the MIFIDPRU 8 Annex 1R template as required. The information contained within this section is as of 31st December 2022.

Composition of regulatory own funds

Own Funds Requirements

An a non-SNI MIFIDPRU Investment Firm, the Firm’s own funds requirement

In line with MIFIDPRU 8.5.1R, the Firm’s own funds requirements as at 30 September 2023 are:

The Firm’s fixed overheads requirement as at 30 September 2023 was £3,957,000. Per the MIFIDPRU TP 2.7(3)(a), MIS own funds requirement is the amount equal to twice the own funds requirement in Chapter 1 of Title I of Part Three of the UK CRR.

The Firm’s 2023 ICARA document was approved by the Board on 22 November 2023.

REMUNERATION

In accordance with the Capital Requirements Regulation remuneration disclosure requirements, as further elaborated in the FCA’s General Guidance on Proportionality: The Remuneration Code (SYSC 19A) & Pillar 3 Disclosures on Remuneration (Article 450 of the Capital Requirements Regulation (CRR)), as an IFPRU limited licence firm the Firm falls within proportionality level 3 and is required to provide the following disclosures regarding its remuneration policy and practices for those categories of staff whose professional activities have a material impact on its risk profile.

The Firm has established a remuneration policy and RemCo in accordance with the FCA’s Remuneration Code. The RemCo comprises two non-executive directors of Multrees. The committee is responsible for overseeing the establishment, implementation and maintenance of remuneration policies, procedures and practices that are consistent with and promote sound and effective risk management. In particular, the committee is responsible for ensuring the Firm’s compliance with the UK FCA’s Remuneration Code, as well as compliance with other applicable laws and regulations, and reports its findings and recommendations to the Board. No external consultant has been used for the determination of the remuneration policy.

Code Staff and Link Between Pay and Performance

The Firm classifies those staff whose professional activities have a material impact on its risk profile as Code Staff in line with the FCA’s Remuneration Code. The firm classified five individuals in total as Code Staff in 2021. The aggregate remuneration paid to the Firm’s Code Staff during the financial year ending on 31 December 2021 was £583,000.

Remuneration comprised base salary, pension contributions and benefits in kind.

Multrees operates a discretionary bonus scheme. The scheme’s purpose was to consider a financial bonus reward if the Company had met financial targets agreed by the Board. Also taken into consideration were personal objectives that had been set and the Company continuing to reduce its exposure to risk. The Bonus paid was variable to each participant depending on their contribution to the Company achieving its financial and risk targets. Awards are cash only. No awards were made in 2021.

There are no code-staff in fee or commission earning roles. There is no minimum pay increase, and no contractual bonuses are in place for current code staff.